When comparing home insurance vs. renters insurance, the decision is not only about cost, but it is also about responsibility, protection, and financial security. Millions of Americans face unexpected financial losses every year due to lack of proper insurance coverage. Many people imagine both policies serving the same purpose, but the reality is different. Each one is designed for a specific living situation and level of risk.

If you own a home, you carry the full financial burden of the property. If you rent, your responsibility is limited to your personal belongings and liability. This difference directly affects the type of insurance you need and how much protection you should have in place.

I think you should choose a better policy that ensures that unexpected events such as fire, theft, or liability claims do not create long-term financial stress. That is why comparing both options in detail is essential before making a decision.

What Does Homeowners Insurance Cover in the USA?

Homeowners insurance is designed to provide full protection for property owners. It covers the structure of the home, personal belongings, and liability risks, making it one of the most important financial tools for homeowners in the United States.

The most important thing about this policy is dwelling coverage, which protects the physical structure of the home. This includes walls, roofs, floors, and built-in systems. If a fire or storm damages your property, this coverage helps pay for repairs or rebuilding. Many homeowners look for more details about home insurance dwelling coverage to ensure they have adequate protection based on their property’s value.

Homeowners insurance typically covers:

- Structural damage to the house (walls, roof, foundation)

- Built-in systems like plumbing, heating, and electrical

- Personal belongings such as furniture and electronics

- Protection against fire, theft, and certain natural disasters

Liability protection is another essential component. If someone is injured on your property, you could face medical bills and legal expenses. This coverage helps manage those costs and protects your finances. If you take insurance for your home protection, then Insurance Centrik provides better guidance for you, like how to check, how to apply, what the benefits are, and how to find affordable rates. We explain everything in simple words according to your budget and insurance-related queries.

Finally, homeowners insurance includes additional living expenses coverage. If your home becomes unlivable, the policy can cover temporary housing, meals, and other necessary expenses while repairs are being completed.

What Does Renters Insurance Cover for Tenants in 2026?

Renters insurance is specifically designed for tenants who do not own the property they live in. In the United States, millions of renters rely on this affordable coverage to protect their belongings and financial well-being. While it does not cover the building itself (that’s the landlord’s responsibility), it provides essential protection for tenants in several important ways.

1. Personal Property Coverage

One of the most valuable parts of renters insurance is personal property coverage. This protects your belongings from sudden incidents like fire, theft, or certain types of water damage.

What’s typically covered:

- Furniture (sofas, beds, tables)

- Electronics (TVs, laptops, smartphones)

- Clothing and shoes

- Kitchen appliances and utensils

- Jewelry and small valuables (limited coverage)

- Bicycles and sports equipment

Many renters underestimate the total value of their belongings. When you add everything up, replacing items after a loss can cost thousands of dollars.

Covered events (named perils) often include:

- Fire and smoke damage

- Theft and vandalism

- Windstorms or hail

2. Liability Protection

Another key feature is liability coverage, which protects you financially if you’re responsible for an accident or damage.

This coverage can help with:

- Medical bills if a guest is injured in your rental

- Legal expenses if someone sues you

- Property damage you accidentally cause to others

Example: If a visitor slips on a wet floor in your apartment and gets injured, renters insurance can help cover medical and legal costs.

3. Additional Living Expenses (ALE) Coverage

If your rental becomes unlivable due to a covered event, renters insurance helps you maintain your lifestyle through additional living expenses coverage.

This may include:

- Hotel or temporary housing costs

- Restaurant meals or food expenses

- Laundry and transportation costs

- Other necessary daily expenses

Example: If a fire damages your apartment, your policy can pay for a hotel stay while repairs are being completed.

What Renters Insurance Does NOT Cover

It’s equally important to understand what renters insurance does not cover:

- The building structure (covered by landlord insurance)

- Flood damage (requires separate flood insurance in the U.S.)

- Earthquake damage (requires separate coverage)

- High-value items beyond policy limits (unless additional coverage is purchased)

Why Renters Insurance Is Important

Renters insurance is one of the most affordable types of coverage in the United States, often costing $10–$25 per month. Despite its low cost, it provides significant financial protection.

Key benefits:

- Protects your belongings from unexpected losses

- Covers liability risks that could cost thousands of dollars

- Provides peace of mind during emergencies

- Often required by landlords or property managers

Although renters insurance does not include structural coverage, it provides important financial protection for tenants at a very affordable cost. From securing your personal belongings to covering liability and temporary living expenses, it plays a crucial role in protecting your financial stability.

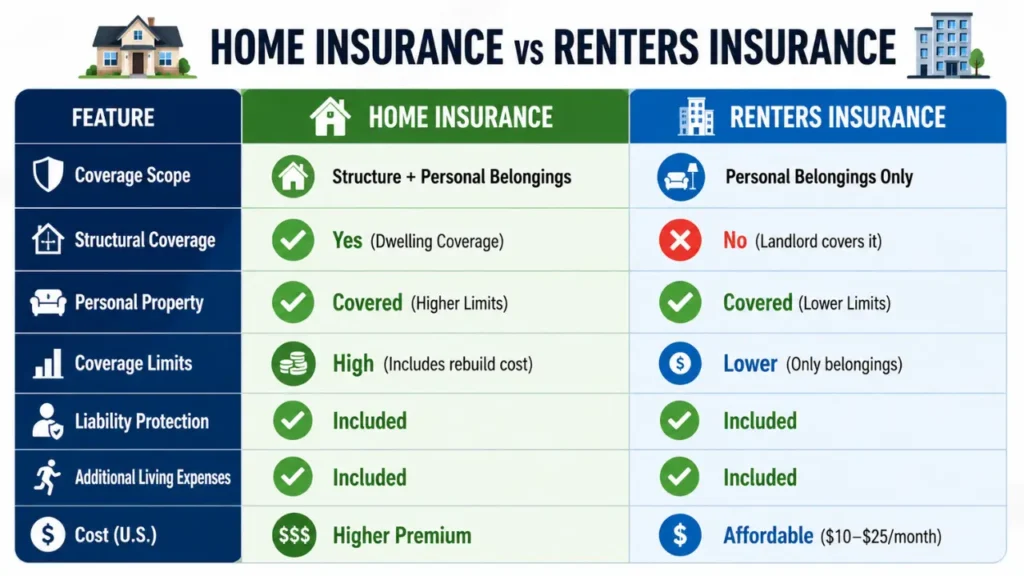

Differences Between Home and Renters Insurance Coverage

It is important to understand the differences between home insurance and renters insurance, as this knowledge is crucial for choosing the appropriate coverage. While both policies provide financial protection, each is designed for a different type of need. Homeowners insurance provides broader protection, including the structure, whereas renters insurance focuses on personal belongings and liability. The comparison below highlights the key differences.

Choosing the right policy depends on whether you own or rent your home and your level of responsibility.

Cost Differences Between Home and Renters Insurance

Cost is one of the biggest factors when comparing Home Insurance vs Renters Insurance. The difference in price reflects the level of coverage provided by each policy.

Here is a clear comparison based on U.S. averages:

| Coverage Type | Home Insurance | Renters Insurance |

| Monthly Premium | $100 – $250 | $10 – $25 |

| Annual Premium | $1,200 – $3,000 | $120 – $300 |

| Structure Coverage | Included | Not Included |

| Personal Property | Included | Included |

| Liability Protection | High Limits | Moderate Limits |

| Additional Living Expenses | Included | Included |

Many users searching renters insurance vs homeowners insurance cost quickly notice how affordable renters insurance is compared to homeowners insurance. This is because renters are not responsible for insuring the structure of the property.

For homeowners, higher premiums are necessary due to the significant cost of repairing or rebuilding a home.

Why Homeowners Insurance Is Essential for Property Owners

Homeowners insurance is very important because it protects one of the largest financial investments most people will ever make. Without proper coverage, any damage caused by fire, storms, or other unexpected events must be paid out of pocket, which can lead to serious financial strain.

Another key reason homeowners insurance is important is lender requirements. In the United States, most mortgage providers require borrowers to maintain active insurance coverage as part of their loan agreement. This ensures that the property remains protected throughout the loan period.

According to the U.S. insurance industry, the average annual cost of homeowners insurance generally ranges from $1,200 to $3,000, depending on factors such as location, property value, coverage limits, and overall risk. While it may seem like an added expense, it is a small price to pay compared to the potential financial loss from major property damage or liability claims.

Understanding the home insurance claim process is also crucial. In the event of damage, knowing how to file a claim, submit proper documentation, and receive compensation can make the recovery process faster, smoother, and less stressful.

Why Renters Insurance Is Important Even If It’s Optional

Many renters assume insurance is unnecessary because they do not own the property, but this can lead to serious financial risks. Personal belongings such as furniture, electronics, and clothing can add up to thousands of dollars in value. Without renters insurance, replacing these items after events like theft or fire can be costly and stressful.

Renters insurance also provides essential liability protection. If a guest is injured in your rental unit or you accidentally cause damage to someone else’s property, you may be responsible for medical bills or legal expenses. Having proper coverage helps protect you from these unexpected financial burdens.

Another key advantage is financial stability and peace of mind. Renters insurance ensures that temporary living expenses, daily costs, and sudden losses do not disrupt your lifestyle. Given its low cost and high value, renters insurance is a smart and practical choice for anyone living in a rental property in the United States.

What Are Key Benefits of Home Insurance vs Renters Insurance?

Both home insurance and renters insurance provide essential protection against losses, but their benefits vary depending on whether you own or rent your home. Choosing the right policy ensures financial stability, risk protection, and a relaxed mind in unexpected situations.

Homeowners Insurance Benefits

Homeowners insurance provides broad coverage because it covers both the property and personal belongings.

Key Advantages:

- Complete Property Protection

- Personal Belongings Coverage

- Higher Liability Limits

- Additional Living Expenses

- Peace of Mind for Homeowners

Renters Insurance Benefits

Renters insurance is a cost-effective solution designed specifically for tenants who want protection without covering the building structure.

Key Advantages:

- Affordable Premiums

- Personal Property Protection

- Liability Coverage

- Additional Living Expenses

- Financial Security at Low Cost

Selecting between home insurance and renters insurance depends on your living situation. Homeowners need broader protection for both their property and belongings, while renters benefit from affordable coverage focused on personal items and liability.

Key Factors That Affect Home and Renters Insurance Costs

Insurance premiums in the United States depend on several important factors. Understanding these elements can help homeowners and renters choose the right coverage while keeping costs under control.

1. Location and Risk Factors

Location is one of the most significant factors affecting insurance costs. Properties in areas prone to natural disasters such as hurricanes, wildfires, floods, or storms typically have higher premiums due to increased risk.

2. Property Value and Coverage Needs

For homeowners, the cost of insurance depends largely on the home’s rebuild value. More expensive homes require higher coverage limits, which increases premiums. For renters, the value of personal belongings plays a similar role.

3. Type of Policy (Home vs Renters)

Home insurance generally costs more because it includes structural coverage, while renters insurance is more affordable since it only covers personal belongings and liability.

4. Credit Score

In many U.S. states, insurance companies use credit-based insurance scores to determine premiums. A higher credit score often leads to lower insurance costs.

5. Security Features

Installing safety features such as burglar alarms, smoke detectors, fire extinguishers, and security systems can reduce premiums by lowering the risk of damage or theft.

6. Claims History

If you have a history of frequent insurance claims, insurers may consider you a higher risk, which can increase your premium.

7. Deductible Amount

The deductible is the amount you pay out of pocket before insurance kicks in. Choosing a higher deductible usually lowers your monthly premium, while a lower deductible increases it.

Insurance costs in the USA depend on multiple factors, including location, property value, and personal risk profile. By improving factors like credit score, home security, and deductible choices, you can effectively reduce your premiums while maintaining the right level of coverage.

How to Choose the Right Home or Renters Insurance Coverage

Choosing the best insurance coverage depends on your living situation, financial responsibilities, and the level of protection you need. Whether you own a home or rent a property, selecting the appropriate policy ensures long-term financial security and peace of mind.

1. Identify Your Living Situation

The first step is understanding whether you need homeowners insurance or renters insurance:

- Homeowners: Require coverage for both the structure and personal belongings

- Renters: Need protection for personal property and liability only

This is the most important factor when deciding between the two policies.

2. Check the Value of Your Assets

Before choosing coverage, calculate the value of what you need to protect:

- Estimate the rebuild cost of your home (for homeowners)

- Calculate the total value of personal belongings (for renters and homeowners)

This helps you select accurate coverage limits and avoid being underinsured.

3. Choose the Right Coverage Limits

Selecting proper coverage limits is essential:

- Avoid choosing limits that are too low, which may not fully cover losses

- Avoid over-insuring, which can increase premiums unnecessarily

Balance your coverage needs with your budget.

4. Compare Policies and Providers

Not all insurance policies are the same. Comparing options helps you find the best value:

- Check policy coverage features and exclusions

- Compare premium costs and deductibles

- Look for discounts and bundled policies

Comparing multiple options ensures better coverage at a competitive price.

5. Review and Update Your Policy Regularly

Your insurance needs can change over time:

- Increase coverage if you buy new valuables or renovate your home

- Update your policy if you move to a new location

- Review annually to ensure your coverage remains relevant

Regular updates prevent gaps in protection.

6. Understand Policy Details Clearly

Always read the fine print before choosing a policy:

- Know what is covered and not covered

- Understand deductibles and claim process

- Be aware of limits on high-value items

This avoids surprises during claims.

Choosing the right home or renters insurance coverage requires careful evaluation of your needs, assets, and risks. By selecting appropriate coverage limits, comparing policies, and reviewing your plan regularly, you can ensure strong protection against losses and long-term peace of mind.

Common Mistakes to Avoid When Buying Insurance

When buying insurance, many people overlook important details that can lead to coverage gaps and financial risks. Failing to assess needs properly, ignoring policy terms, or not updating coverage over time can reduce protection. Understanding these common mistakes helps ensure your insurance remains reliable and effective.

Key Mistakes:

- Not checking the real value of your belongings

- Not reading what the policy does not cover

- Selecting the cheapest plan without checking benefits

- Forgetting to update the policy after changes

- Choosing too little or too much coverage

Home vs. Renters Insurance – Which One Is Best for You?

When deciding between home insurance and renters insurance, the most important factor is whether you own or rent your property. Each policy is designed to meet different needs, so selecting the right one depends on your level of responsibility and the type of protection required.

Home insurance provides stronger financial protection because it includes structural coverage, higher liability limits, and support for rebuilding costs. On the other hand, renters insurance is a practical and affordable option for tenants who want to protect their personal items and stay financially secure.

Overall, having the right insurance coverage ensures you are prepared for unexpected events. Making an informed choice helps protect your finances, reduce risks, and maintain peace of mind in the long run.

FAQs

How much does homeowners insurance cost per month?

On average, homeowners insurance costs between $100 and $250 per month in the United States. However, the actual cost depends on location, property value, coverage limits, deductible, and the overall risk associated with the area.

Does renters insurance cover natural disasters?

It depends on the policy. Most renters insurance plans cover disasters like fire, storms, and smoke damage. However, floods and earthquakes are usually excluded and require purchasing separate coverage or additional policy endorsements.

What does homeowners insurance cover?

Homeowners insurance covers the physical structure of your home, personal belongings, liability risks, and additional living expenses if your home becomes uninhabitable. It provides comprehensive financial protection against common risks and unexpected damages.

When should you switch from renters to homeowners insurance?

You should switch when you purchase a home and become responsible for the property structure. At that point, homeowners insurance is essential to protect your investment, cover damages, and provide liability protection for long-term financial security.

Aarvith is the author and founder of Insurance Centrik. He researches various insurance topics, including auto, health, travel, home, and business insurance. He provides accurate insurance information from reliable sources and industry expertise.